SOLUTION: You plan to work for 40 years and then retire using a 25-year annuity. You want to arrange a retirement income of $4700 per month. You have access to an account that pays an APR of

Algebra ->

Customizable Word Problem Solvers

-> Finance

-> SOLUTION: You plan to work for 40 years and then retire using a 25-year annuity. You want to arrange a retirement income of $4700 per month. You have access to an account that pays an APR of

Log On

Question 1009196: You plan to work for 40 years and then retire using a 25-year annuity. You want to arrange a retirement income of $4700 per month. You have access to an account that pays an APR of 7.2% compounded monthly.

What size nest egg do you need to achieve the desired monthly yield? (Round your answer to the nearest cent.) Answer by Theo(13342) (Show Source):

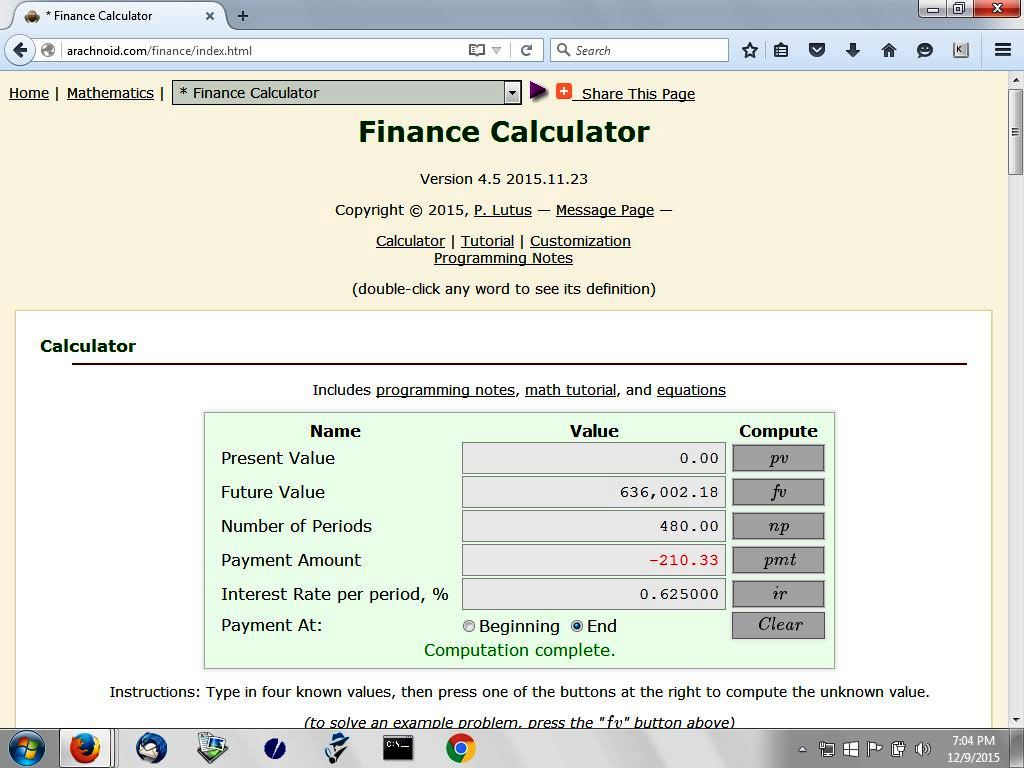

You can put this solution on YOUR website! a 25 year annuity account at 7.5% compounded monthly delivering 4700 per month has a present value of 636,002.18

that would be the value of the nest egg that you would need in 40 years.

assuming you can invest monthly starting now to ensure that you would have 4700 per month for 25 years after you retire, you would need to invest 210.33 per month for for the next 40 years.

assumptions:

money is invested or withdrawn at the end of each month.

monthly interest rate used is the annual interest rate divided by the number of compounding periods.

7.5% per year becomes .625% per month.

interest earned during the 40 month investment period becomes part of the principal that interest is earned on.

in other words, it is reinvested in the account.

account balance in the 25 month withdrawal period continues to earn interest as long as it remains in the account.

the calculations were done using the following online financial calculator.

here's the calculator results for the 40 year investment period.

here's the calculator results for the 25 year withdrawal period.

the inputs are in black.

the results are in red.

in the first calculation we were looking for the monthly investment.

in the second calculation we were looking for the present value of the monthly withdrawal.

disregard negative signs.

they mean something, but not in the context of how we used the calculator to provide our results.