SOLUTION: your goal is to create a college fund for your child, suppose you find a fund that offers an Apr of 6%. How much money should you deposit monthly to accumulate $85,000 in 17 years

Algebra ->

Customizable Word Problem Solvers

-> Finance

-> SOLUTION: your goal is to create a college fund for your child, suppose you find a fund that offers an Apr of 6%. How much money should you deposit monthly to accumulate $85,000 in 17 years

Log On

Question 1098818: your goal is to create a college fund for your child, suppose you find a fund that offers an Apr of 6%. How much money should you deposit monthly to accumulate $85,000 in 17 years Answer by Theo(13342) (Show Source):

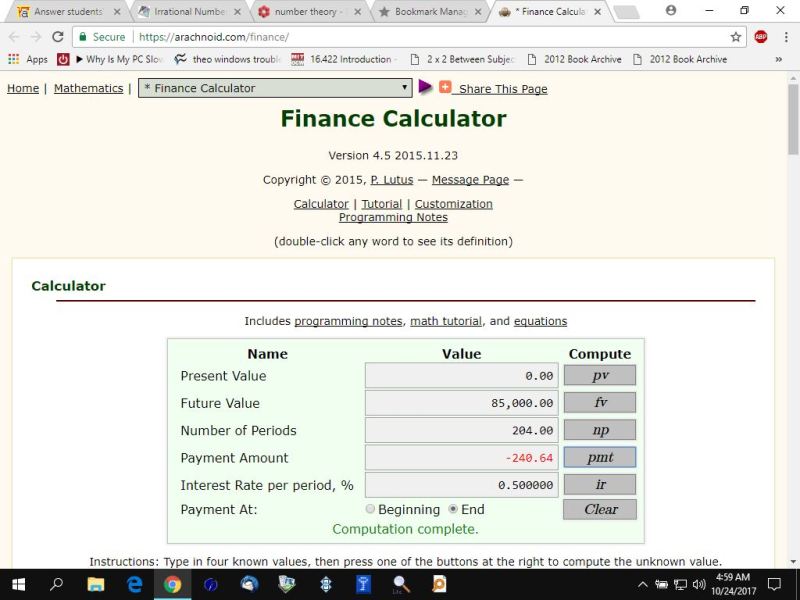

you can also get the same result using the following formula.

ANNUITY FOR A FUTURE AMOUNT WITH END OF TIME PERIOD PAYMENTS

a = (f*r)/((1+r)^n-1)

a is the annuity.

f is the future amount.

r is the interest rate per time period.

n is the number of time periods.

f = 85000

r = .06/12 = .005

n = 17*12 = 204

a = (f*r)/((1+r)^n-1) becomes:

a = (85000*.005)/((1.005)^204-1)

solve for a to get a = 240.6356536

all the calculators used agree and the manually constructed formula agrees as well.

note that the formula requires decimal equivalent of percent which you derive by dividing percent by 100.

not also that the calculator requires either payment to be positive and future value to be negative or vice versa.

this has to do with cash flow concentions.

in this case, payment was money going out to the bank and future value was money coming back from the bank, therefore payment is negative and future value is positive.

some calculator will convert from yearly periods to monthly periods for you.

these calculator and the formula don't so you have to do it yourself.

since your compounding periods were monthly, then all had to be converted to monthly amounts.

17 years * 12 months per year = 204 months.

6% divided by 12 = .5% per month.

decimal equivalent of .5% per month = .5%/100% = .005