Tutors Answer Your Questions about Money Word Problems (FREE)

Question 284285: Hi! I need to ask help for this problem. The answer that I got was $1,200, and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder. Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A. At this rate, how much is the total value of the mill?

Found 2 solutions by n2, ikleyn:

Answer by n2(79)  (Show Source): (Show Source):

You can put this solution on YOUR website! .

Hi! I need to ask help for this problem. The answer that I got was $1,200,

and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder.

Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A.

At this rate, how much is the total value of the mill?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

let the value of the mill be 'x'.

A owned 3/5*x = 3x/5

B owned 2/5*x= 2x/5

After the deal, the part of mr.A is 3x/5 - 1200 dollars; the part of mr.B is 2x/5 + 1200 dollars.

Therefore, the "equality" equation after the deal is

3x/5 - 1200 = 2x/5 + 1200

Simplify and find 'x'

x/5 = 2400

x = 12000.

ANSWER. The total value of the mill is $12000.

Solved.

Answer by ikleyn(53748)  (Show Source): (Show Source):

You can put this solution on YOUR website! .

Hi! I need to ask help for this problem. The answer that I got was $1,200,

and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder.

Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A.

At this rate, how much is the total value of the mill?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect,

since he incorrectly interpreted the problem and incorrectly setup the governing equation.

Below is my complete correct solution

let the value of the mill be 'x'.

A owned 3/5*x = 3x/5

B owned 2/5*x= 2x/5

After the deal, the part of mr.A is 3x/5 - 1200 dollars; the part of mr.B is 2x/5 + 1200 dollars.

Therefore, the "equality" equation after the deal is

3x/5 - 1200 = 2x/5 + 1200

Simplify and find 'x'

x/5 = 2400

x = 12000.

ANSWER. The total value of the mill is $12000.

Solved correctly.

Nice problem, and it deserves to be solved correctly and instructively.

Question 282321: A jogger started a course at 4.5 mph. A cyclist started the same course 1 hour later at an average speed of 14 mph. How long after the jogger started did the cyclist take over the jogger? Round to the nearest tenth of an hour.

Found 3 solutions by greenestamps, josgarithmetic, ikleyn:

Answer by greenestamps(13327)  (Show Source): (Show Source):

You can put this solution on YOUR website!

When the cyclist starts, the jogger has been running for an hour at 4.5 mph, covering a distance of 4.5 miles.

The rate at which the cyclist catches up to the jogger is the difference in their rates, which is 14-4.5 = 9.5 mph.

The time required for the cyclist to catch up to the jogger is the catch-up distance divided by catch-up the rate, which is 4.5/9.5 = 9/19 hours.

The question asks for the time after the jogger starts for the cyclist to catch up to the jogger; that is 1 + 9/19 = 28/19 hours.

28/19 = 1.4736...

Rounded to the nearest tenth of an hour, per the instructions...

ANSWER: 1.5 hours

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

Question 279618: Investor Company loaned out a total of $36,000, part at 6% interest and part at 9% interest. They reported that the annual earnings from both investments were the same amount that would have been earned by the total loan if it had been invested at 8%. Find the amount loaned at each rate.

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Investor Company loaned out a total of $36,000, part at 6% interest and part at 9% interest.

They reported that the annual earnings from both investments were the same amount that would have been earned

by the total loan if it had been invested at 8%. Find the amount loaned at each rate.

~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect,

since the governing equation was setup incorrectly in his post.

I came to bring a correct and accurate solution.

Let x be the amount invested at 9% interest.

Then (36000-x) dollars invested at 6%.

Write the total interest equation

0.09x + 0.06*(36000-x) = 0.08*36000.

Simplify and find x

0.09x + 0.06*36000 - 0.06x = 0.08*36000,

0.09x - 0.06x = 0.08*36000 - 0.06*36000,

0.03x = 0.02*36000

x =  = 24000.

ANSWER. $24000 was invested at 9% and the rest, 36000-24000 = 12000 dollars, was invested at 6%.

CHECK. The total interest is 0.09*24000 + 0.06*12000 = 2880 dollars.

Calculated by another way, it is 0.08*36000 = 2880 follars, the same amount.

The solution is confirmed to be correct. = 24000.

ANSWER. $24000 was invested at 9% and the rest, 36000-24000 = 12000 dollars, was invested at 6%.

CHECK. The total interest is 0.09*24000 + 0.06*12000 = 2880 dollars.

Calculated by another way, it is 0.08*36000 = 2880 follars, the same amount.

The solution is confirmed to be correct.

Solved correctly.

Question 268809: if the U.S grows at an annual rate of 7.5%, how long will take to reach a population of 400 000 000?(the population, now, is 300 000 000)

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

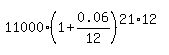

Question 1210582: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

Found 2 solutions by MathTherapy, josgarithmetic:

Answer by MathTherapy(10806)  (Show Source): (Show Source):

You can put this solution on YOUR website!

At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other

deposits or withdrawals are made during this period?

The value of the account will be $?

****************************

Answer by josgarithmetic(39792) (Show Source):

Question 1210581: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

Found 2 solutions by ikleyn, timofer:

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Money_Word_Problems/1210581: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday,

assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

~~~~~~~~~~~~~~~~~~~~~~~~~~

First birthday is after 1 year from the day of the birth.

Second birthday is after 2 years from the day of the birth.

. . . . . . . .

21-th birthday is after 21 year from the day of the birth.

So, the question is about the Future value of the deposit after 21 year.

The formula to calculate is

FV =  = 38658.08 dollars (rounded).

ANSWER. Future value at the twenty-first birthday will be 38,658.08 dollars. = 38658.08 dollars (rounded).

ANSWER. Future value at the twenty-first birthday will be 38,658.08 dollars.

Solved.

Answer by timofer(155) (Show Source): (Show Source):

Question 1000209: A man invests his savings in two accounts, one paying 6 percent and the other paying 10 percent simple interest per year.

He puts twice as much in the lower-yielding account because it is less risky. His annual interest is 3960 dollars.

How much did he invest at each rate?

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

A man invests his savings in two accounts, one paying 6 percent and the other paying 10 percent simple interest per year.

He puts twice as much in the lower-yielding account because it is less risky. His annual interest is 3960 dollars.

How much did he invest at each rate?

~~~~~~~~~~~~~~~~~~~~~~~~~~~

The answer in the post by @mananth, 10,000 at 10% and 20,000 at 6%, is incorrect

I came to bring a correct solution.

investment in 10% --------x

Investment in 6% ----------2x

10%x+6%(2x) = 3960

multiply by 100

10x + 12x = 396000

22x = 396000

x = 396000/22

x=18000

ANSWER. 18,000 at 10% and 36,000 at 6%

CHECK. 0.1*18000 + 0.06*(2*18000) = 3960. ! correct !

Solved correctly.

Question 1188420: a) A total of $40,000 was invested, part of it at 12% interest and the remainder at 15%.

If the total yearly interest from both investments was $5,800. How much was invested at each rate

Answer by josgarithmetic(39792) (Show Source):

Question 592081: A total of $5,000 was invested, part of it at 5 % interest and the remainder at 7 %. If the total yearly interest amount is $325 , how much was invested at 5 %?

Answer by josgarithmetic(39792) (Show Source):

Question 1028742: Mr. Cantoni invested 50,000.00. A part of it is invested in a bank at 2% yearly interest and another part of it in a mutual fund at a 5% yearly interest. How much investment was made in the mutual fund if his yearly income from the two is 2,800.00?

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39792) (Show Source):

You can put this solution on YOUR website!

RATE% QUANTITY INTEREST

Bank 2 50000-Q 0.02(50000-Q)

Mutual F. 5 Q 0.05Q

TOTAL 50000 2800

You can setup the equation and solve, but the results will not work!

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Mr. Cantoni invested 50,000.00. A part of it is invested in a bank at 2% yearly interest and another part of it

in a mutual fund at a 5% yearly interest. How much investment was made in the mutual fund if his yearly income

from the two is 2,800.00?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The problem has no adequate solution, since it is self-contradictory and describes a situation

which can not happen in reality.

Indeed, the claimed income of 2,800.00 is greater that 5% of the total sum of 50,000.00.

So, even if the whole amount of 50,000.00 is invested at 5%, it can not generate 2,800.00.

@mananth in his post solved the problem using his computer code, but obtained one deposit NEGATIVE,

which is not possible in real life.

He did not notice this absurdism and presented negative investment as the solution

to the problem.

This once again shows how dangerous it is to trust the solutions by @mananth.

He even does not read the solutions produced by his computer code and does not check them.

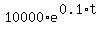

Question 33003: A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and continous compounding, what is the answer?

Found 2 solutions by n2, ikleyn:

Answer by n2(79) (Show Source):

You can put this solution on YOUR website! .

A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and

continuous compounding, what is the answer?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The formula for the future value at continuous compounding is

FV =  , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 = , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 =  .

It implies .

It implies

= =  ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t = ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t =  = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions. = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions.

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and

continuous compounding, what is the answer?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by the other tutor is fatally incorrect.

I came to bring a correct solution.

The formula for the future value at continuous compounding is

FV = , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 = .

It implies

= ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t = = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions.

Solved correctly with complete explanations.

Question 1177589: After what period is the interest generated equal to the original principal if the account pays 6% compounded daily?

Answer by ikleyn(53748) (Show Source):

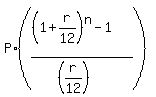

Question 1158170: lee deposits $200 every month into a savings account that earns 3.25% compounded monthly. how many years would it take lee to reach his savings goal of $9000. keep 2 decimal places in your final anwser.

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Lee deposits $200 every month into a savings account that earns 3.25% compounded monthly.

How many years would it take lee to reach his savings goal of $9000. keep 2 decimal places in your final anwser.

~~~~~~~~~~~~~~~~~~~~~~~~~

First, I will solve this problem.

After finishing my solution, I will discuss on how the problem is posed, worded,

and what I think about all of this.

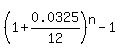

Use a standard formula for the future value of an ordinary annuity compounded monthly

FV =  where FV is the future value, P is the payment at the end of each month,

r is the nominal interest rate per year expressed as decimal,

n is the number of monthly deposits (of months).

So, we need to find " n " from this equation

where FV is the future value, P is the payment at the end of each month,

r is the nominal interest rate per year expressed as decimal,

n is the number of monthly deposits (of months).

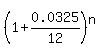

So, we need to find " n " from this equation

= =  = =  = 45, = 45,

= =  .

Rewrite it in this form

= 0.121875, .

Rewrite it in this form

= 0.121875,

= 1 + 0.121875 = 1.121875.

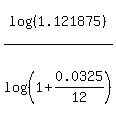

Take logarithm base 10 of both sides

n*log(1+0.0325/12) = log(1.121875)

and calculate

n = = 1 + 0.121875 = 1.121875.

Take logarithm base 10 of both sides

n*log(1+0.0325/12) = log(1.121875)

and calculate

n =  = 42.51952746 months.

Now we should round it to the closest greater integer number of months, which is 43 months,

in order for the bank would be in position to perform the last compounding at the end of the 43-th month.

43 months is the same as 3 years and 7 months.

ANSWER. The amount will exceed the goal of $9,000 in 43 months, or 3 years and 7 months. = 42.51952746 months.

Now we should round it to the closest greater integer number of months, which is 43 months,

in order for the bank would be in position to perform the last compounding at the end of the 43-th month.

43 months is the same as 3 years and 7 months.

ANSWER. The amount will exceed the goal of $9,000 in 43 months, or 3 years and 7 months.

Solved.

-------------------------

The instruction to this problem, saying " keep 2 decimal places in your final answer ", is incorrect and non-sensical.

The answer to this problem should be expressed as an integer number of months.

Since the instruction is incorrect and non-sensical, it tells me that a person who created this problem,

is (1) unprofessional Math writer/composer and (2) is a random person in this field.

He or she is still able to re-write from other sources, but does not understand the meaning of the problem

and does not really understand what he/she writes or re-writes. It is very sad to me to see it and to tell it.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have been solving problems on this forum for many years.

I've seen dozens similar problems like

"how long does it take for a discretely compounded account to get an assigned value".

and I myself have probably solved about fifteen such problems at this forum.

But I have never seen such a problem formulated correctly at the forum.

They always asked for a final result "with two decimal places," which is meaningless in such problems,

where the final answer MUST be expressed in integer number of compounding periods.

Okay, I know, and you don't need to explain or refute it to me, that most of the incoming tasks

are intended for use as solutions on other websites or as a knowledge base for artificial intelligence.

But then, dear managers, you must ensure that you employ the most highly qualified people in the field.

However, what I see in the example of this task tells me the opposite - some of your employees do not meet

the high standards required for creating artificial intelligence.

And this is not just anywhere, but in the crucial matter of correctly formulating

the problem statement, where everything must be perfectly smooth and accurate.

Question 1201069: You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly. How much money will you have on June 30, 2006?

Found 3 solutions by MathTherapy, CPhill, ikleyn:

Answer by MathTherapy(10806) (Show Source):

You can put this solution on YOUR website!

You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly. How much

money will you have on June 30, 2006?

CAN'T believe those 2 "respondents" rounded too early, as usual, and both came up the same WRONG answr: $5,981.

Is this some kind of mutiny? One AI respondent replicating another's WRONG answer and maybe trying to "drum" up

support for each other's ineptitude?

Formula for the FUTURE VALUE of $1:  , where: , where:

= Accumulated amount/FUTURE VALUE (UNKNOWN, in this case) = Accumulated amount/FUTURE VALUE (UNKNOWN, in this case)

= Present Value, or Principal invested, or INITIAL amount deposited/Invested ($5,000, in this case) = Present Value, or Principal invested, or INITIAL amount deposited/Invested ($5,000, in this case)

= Annual Interest rate (2.75%, or .0275, in this case) = Annual Interest rate (2.75%, or .0275, in this case)

= Number of ANNUAL compounding periods (monthly, or 12, in this case) = Number of ANNUAL compounding periods (monthly, or 12, in this case)

= Time, in years ( = Time, in years ( , in this case)

becomes: , in this case)

becomes:  , and then FUTURE VALUE, or , and then FUTURE VALUE, or

Answer by CPhill(2189)  (Show Source): (Show Source):

You can put this solution on YOUR website! r = R/100

r = 2.75/100

r = 0.0275 rate per year

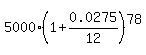

Amount A = P(1 + r/n)nt

A = 5,000.00(1 + 0.0275/12)^((12)(6.5))

A = 5,000.00(1 + 0.0023)^(78)

A=$5981

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly.

How much money will you have on June 30, 2006?

~~~~~~~~~~~~~~~~~~~~~~~

Calculations and the answer in the post by @mananth are incorrect.

I came to make the job accurately as it should be done.

r = R/100

r = 2.75/100

r = 0.0275 rate per year

Amount A =  , N is the number of compounding (= the same as the number of months N = 78).

A = , N is the number of compounding (= the same as the number of months N = 78).

A =  A = $5977.39. ANSWER

A = $5977.39. ANSWER

Solved correctly.

-------------------------

These typical financial problems assume a PRECISE solution correct to one single cent.

It is a standard for banking practice, and it is a standard for solving school/college exercises

in Financial Math, because the answer of an exercise must match to the precise standard value.

To get a precise answer, NEVER make intermediate rounding, since it inevitably leads to loosing precision.

To get a precise answer, use specialized financial calculators, or specialized online calculators,

or Excel spreadsheets.

Question 1201119: Sara deposited $1400 for 1 year at 10%, compound semiannually.

b. What percent interest was added each time?

c. What was the balance in Sara's account at the end of 1 year?

Answer by ikleyn(53748) (Show Source):

Question 1164876: A dealer has PKR 100 million and receives the following rates of foreign exchange from the market. Find out how dealer can earn maximum arbitrage profit in FX market transaction. Solve and explain step by step.

USD/PKR 138/139

GBP/PKR 199/201

GBP/USD 1.2729/35

EUR/GBP 1.1520/33

Answer by CPhill(2189) (Show Source):

You can put this solution on YOUR website! To determine if an arbitrage opportunity exists, we need to compare the **direct rates** (provided by the market) with the **cross rates** (calculated using other currency pairs). Arbitrage is possible if the cross rate is significantly different from the market rate, allowing us to "buy low" in one market and "sell high" in another.

Since we are starting with **PKR 100 million**, we are looking for a **Triangular Arbitrage** path.

---

### Step 1: Analyze the Market Rates (Bid/Ask)

The rates are given as **Bid / Ask**.

* **Bid:** The rate at which the bank buys the base currency (left side).

* **Ask:** The rate at which the bank sells the base currency (left side).

| Pair | Bid (Bank Buys) | Ask (Bank Sells) |

| --- | --- | --- |

| **USD/PKR** | 138.00 | 139.00 |

| **GBP/PKR** | 199.00 | 201.00 |

| **GBP/USD** | 1.2729 | 1.2735 |

---

### Step 2: Calculate the Implied Cross Rate

Let's see what the GBP/PKR rate *should* be based on the USD/PKR and GBP/USD rates.

**Comparison:**

* The market **GBP/PKR Ask** is **201.00**.

* Our calculated **Implied Ask** is **177.0165**.

* The market **GBP/PKR Bid** is **199.00**.

Because the market's Bid for GBP (199.00) is much higher than the cost to "create" a GBP through USD (177.0165), an arbitrage opportunity exists. We should buy GBP using the USD route and sell it directly for PKR.

---

### Step 3: Execute the Arbitrage Path

The goal is to go: **PKR USD GBP PKR**.

**1. Convert PKR to USD:**

We must buy USD from the bank at the **Ask** rate (139.00).

**2. Convert USD to GBP:**

We need to buy GBP. The rate GBP/USD is 1.2729/35. The bank sells GBP at the **Ask** (1.2735).

**3. Convert GBP back to PKR:**

We sell our GBP to the market at the **GBP/PKR Bid** rate (199.00).

---

### Step 4: Calculate the Profit

* **Ending PKR:** 112,418,898.91

* **Starting PKR:** 100,000,000.00

* **Total Profit:** **PKR 12,418,898.91**

The dealer earns a profit of approximately **12.42%** in one cycle.

---

### Summary Table of Transactions

| Action | Currency Pair used | Rate | Result |

| --- | --- | --- | --- |

| **Start** | PKR | — | 100,000,000.00 |

| **Sell PKR for USD** | USD/PKR (Ask) | 139.00 | 719,424.46 |

| **Sell USD for GBP** | GBP/USD (Ask) | 1.2735 | 564,919.09 |

| **Sell GBP for PKR** | GBP/PKR (Bid) | 199.00 | 112,418,898.91 |

**Note on EUR/GBP:** The rate EUR/GBP 1.1520/33 was provided but not needed for this specific triangular loop. It would only be used if we were attempting a four-way arbitrage involving the Euro.

Would you like me to check if adding the Euro into the cycle (PKR USD GBP EUR PKR) would yield a higher profit?

Question 1164972: A major shipping company is planning to purchase new cargo ships. It wants to borrow $1100 million by issuing bonds. The bonds are for a 15-year period with at a rate of 9 percent per year compounded quarterly. Interest is to be paid each quarter to bondholders. How much will the company have to pay in quarterly interest? How much interest will it pay over the 12-year period?

Answer by CPhill(2189) (Show Source):

You can put this solution on YOUR website! ```python

principal = 1100 * 10**6

annual_rate = 0.09

compounding_frequency = 4

years_period = 12

quarterly_rate = annual_rate / compounding_frequency

quarterly_interest = principal * quarterly_rate

total_quarters_12_years = years_period * compounding_frequency

total_interest_12_years = quarterly_interest * total_quarters_12_years

print(f"{quarterly_interest=}")

print(f"{total_interest_12_years=}")

```

```text

quarterly_interest=24750000.0

total_interest_12_years=1188000000.0

```

To calculate the interest payments for the shipping company's bonds, we use the simple interest formula applied to each compounding period (quarter), as the interest is paid out to bondholders.

### 1. Quarterly Interest Payment

The quarterly interest rate is the annual rate divided by the number of quarters in a year.

* **Principal ():**

* **Annual Rate ():**

* **Quarters per year ():**

**The company will have to pay $24.75 million in quarterly interest.**

---

### 2. Interest Paid Over a 12-Year Period

To find the total interest over 12 years, we multiply the quarterly payment by the total number of quarters in that timeframe.

* **Number of Quarters:**

**The company will pay $1,188 million (or $1.188 billion) in interest over the 12-year period.**

Question 448368: Jim opens a savings account with a deposit of $10,000. If the account has an annual interest rate of 6%, compounded quarterly, how much is in the account after one year.

Can you show me steps on how to work this problem. It's been years since I had algebra. Thank you so much.

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Jim opens a savings account with a deposit of $10,000. If the account has an annual interest rate of 6%,

compounded quarterly, how much is in the account after one year.

Can you show me steps on how to work this problem. It's been years since I had algebra. Thank you so much.

~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @manant is presented incorrectly/inaccurately.

I came to bring a correct/accurate solution in the form as it SHOULD be presented.

Principal P = 10,000

Amount = A

years = 1

compounded 4 times a year

Rate = 6% = 0.06.

Amount =  = =  = 10613.64. ANSWER = 10613.64. ANSWER

Solved.

Question 442367: 20000$ is split into two investments one paying 5% and the other paying 6.5% to the nearest cent how much should be invested in each so the yearly intrest from the 5% investment is double the intrest from 6.5% investment

Found 2 solutions by timofer, ikleyn:

Answer by timofer(155) (Show Source):

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

20000$ is split into two investments one paying 5% and the other paying 6.5%. To the nearest cent how much should be

invested in each so the yearly interest from the 5% investment is double the interest from 6.5% investment

~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect due to arithmetic error.

Below is my correct solution.

let investment at 6.5% be x.

Investment at 5% is (20000-x).

...

0.05*x = 2*0.065*(20000-x)

Multiply by 100 both sides of the equation

5x = 2*6.5(20000-x)

5x = 260000 - 13x

18x = 260000

x = 260000/18 = 14,444.44 dollars invested at 6.5%.

The rest, or 20,000 - 14,444.44 = 5,555.56 dollars invested at 5%.

CHECK. The interest of the 5% investment is 14444.44*0.05 = 722.22.

The interest of the 6.5% investment is 0.065*5555.56 = 361.11.

The interest of the 5% investment is the doubled interest of the 6.5% investment. ! correct !

Solved correctly.

Question 436823: How long does it take $875 to double if it is invested at 8% compounded monthly?

Found 4 solutions by MathTherapy, n3, josgarithmetic, ikleyn:

Answer by MathTherapy(10806) (Show Source):

You can put this solution on YOUR website!

How long does it take $875 to double if it is invested at 8% compounded monthly?

Future value of $1 formula:  Doesn't matter what P is, A will ALWAYS be 2 (DOUBLE).

So, substituting 2 for A (Accumulated amount/Future Value), 1 for P (Principal, or Initial Investment/Amount), .08 for

i (interest rate, as a percent/decimal), 12 for m (number of annual coumpounding periods), t (time, in years) is UNKNOWN.

With that, now becomes:

Doesn't matter what P is, A will ALWAYS be 2 (DOUBLE).

So, substituting 2 for A (Accumulated amount/Future Value), 1 for P (Principal, or Initial Investment/Amount), .08 for

i (interest rate, as a percent/decimal), 12 for m (number of annual coumpounding periods), t (time, in years) is UNKNOWN.

With that, now becomes:

----- Converting to LOGARITHMIC form

Time, or ----- Converting to LOGARITHMIC form

Time, or  , or approximately 8.693189 years, or 8 years, 8.3183 months, or 104.3183 months.

This amount is then ROUNDED to a time of 105 months, or 8 years, and 9 months.

As stated by Tutor @IKLEYN, the 8.3183 years, or 104.3813 months MUST be ROUNDED UP to the next INTEGER, which is 105.

Note that at the 104th-month, or 8-year, 8-month juncture, the amount will NOT have doubled. One has to wait until the 105th

month to see the invested amount DOUBLE. , or approximately 8.693189 years, or 8 years, 8.3183 months, or 104.3183 months.

This amount is then ROUNDED to a time of 105 months, or 8 years, and 9 months.

As stated by Tutor @IKLEYN, the 8.3183 years, or 104.3813 months MUST be ROUNDED UP to the next INTEGER, which is 105.

Note that at the 104th-month, or 8-year, 8-month juncture, the amount will NOT have doubled. One has to wait until the 105th

month to see the invested amount DOUBLE.

Answer by n3(7) (Show Source): (Show Source):

You can put this solution on YOUR website! .

The post by @josgarithmetic with his answer " about 8 years and 8 months " is

(1) incorrect

and

(2) distorts the meaning of the problem and the meaning of my solution.

This problem is not seeking for an approximate solution.

What josgarithmetic calls " an approximate solution ", is NOT a solution and is NOT an appropriate solution.

The problem seeks for a PRECISE solution, instead, which is achieved via the proper rounding.

The proper rounding of the resulting decimal number to the closest greater integer number

is an integral and essential part of the solution, which can not be neglected/ignored/omitted.

Regarding all the rest in the post by @josgarithmetic, it is a reduced re-writing from the solution by @ikleyn.

Therefore, my advise and instruction to a reader is fully ignore the post by @josgaritmetic.

*********************************************************************

@josgarithmetic, rewriting from others is a very low-level practice,

so I advise you to stop doing it.

*********************************************************************

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

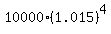

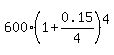

Question 434949: What will be the future value in a year if $600 is invested at a rate of 15% compounded quarterly

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

What will be the future value in a year if $600 is invested at a rate of 15% compounded quarterly

~~~~~~~~~~~~~~~~~~~~~~~~~

The answer in the post by @mananth is correct, but his intermediate formulas are wrong.

Wrong formulas in his post can confuse a reader.

To avoid confusing, I place my solution here in the form as it SHOULD be presented.

Principal P = 600

years = 1

compounded 4 times a year

Rate = 15% which means that the effective rate is  per quarter.

Future value = per quarter.

Future value =  Amount =

Amount =  = 695.19 dollars.

ANSWER. Future value in a year is $695.19. = 695.19 dollars.

ANSWER. Future value in a year is $695.19.

Solved and presented correctly.

----------------------

Again, I placed this my solution here to OVERLAY wrong formulas in the post by @mananth.

///////////////////////////

I notice that it is just second time I see this inaccurate writing in a post by @mananth.

First time I noticed it under link

https://www.algebra.com/algebra/homework/word/finance/Money_Word_Problems.faq.question.432879.html

From these coincidences, and from many other coincidences that I saw, I conclude

that @mananth is not really a person (not a human), but a computer code (like a very early version

of an Artificial Intelligence), which generates all the posts/solutions under his nickname.

Simply, for his calculations, he (or it) uses a code with two decimals

for printing real numbers, which produces this permanent error in his posts.

So, similar to as @CPhill was a pseudonym for the AI version of January 2025,

exactly in the same way @mananth is a pseudonym for more earlier (and more primitive) version of AI.

It is a computer code, in short.

Question 432879: final amount of the investment if $8000 invested at 6% compounded quarterly for 6 years

Answer by ikleyn(53748) (Show Source):

Question 419077: Dave Horn invested half of his money at 5%, one-tird of his money at4%, and the rest at 3.5%. If his total annual investment incomw is $530, how much had he invested?

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

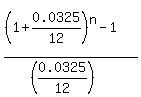

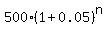

Question 729539: Alison deposits $500 into a new savings account that earns 5 percent interest compounded annually. If Alison makes no additional deposits or withdrawals, how many years will it take for the amount in the account to double?

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Alison deposits $500 into a new savings account that earns 5 percent interest compounded annually.

If Alison makes no additional deposits or withdrawals, how many years will it take for the amount

in the account to double?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

We start from the standard formula for the future value of a compounded account

FV =  .

We write this equation for the doubled future value

1000 = .

We write this equation for the doubled future value

1000 =  .

Here 'n' is the unknown number of the years (= number of compounding) to find.

We simplify equation (1) step by step .

Here 'n' is the unknown number of the years (= number of compounding) to find.

We simplify equation (1) step by step

= =  .

2 = .

Take logarithm of both sides

log(2) = n*log(1.05).

Express and calculate 'n'

n = .

2 = .

Take logarithm of both sides

log(2) = n*log(1.05).

Express and calculate 'n'

n =  = 14.21 (approximately).

The number of compounding is an integer number - so, we must round this decimal 14.21

to the closest GREATER integer 15 in order for the bank be in position to make the last compounding.

ANSWER. First time the compounded amount will exceed the doubled principal in 15 years. = 14.21 (approximately).

The number of compounding is an integer number - so, we must round this decimal 14.21

to the closest GREATER integer 15 in order for the bank be in position to make the last compounding.

ANSWER. First time the compounded amount will exceed the doubled principal in 15 years.

Solved.

---------------------

The solution/answer in the post by @lynnlo both are incorrect,

so, ignore his post for the peace in your mind.

/\/\/\/\/\/\/\/\/\/\/\/

I N T E R E S T I N G

I checked today, on December 15, 2025, how Artificial Intelligence, Google AI Overview

treats this problem.

It produces the same answer 14.2 years as in the post by @lynnlo, without any critical analysis,

i.e., treats the problem INCORRECTLY.

I copied all references from the Google AI Overview output they are copy-pasted below.

[1] https://www.gauthmath.com/solution/1806082773471301/How-long-will-it-take-money-to-double-itself-if-invested-at-5-compounded-annuall

[2] https://askfilo.com/user-question-answers-smart-solutions/7-determine-how-long-will-it-take-money-to-double-itself-if-3331353538313435

[3] https://www.nerdwallet.com/banking/calculators/compound-interest-calculator

[4] https://study.com/skill/learn/finding-the-final-amount-in-a-word-problem-on-compound-interest-explanation.html

[5] https://www.vaia.com/en-us/textbooks/math/excursions-in-modern-mathematics-8-edition/chapter-10/problem-27-find-the-apr-of-a-bond-that-doubles-its-value-in-/

[6] https://askfilo.com/user-question-answers-smart-solutions/at-what-rate-a-sum-of-money-will-be-doubled-in-20-years-3133353733363230

[7] https://www.vaia.com/en-us/textbooks/math/contemporary-precalculus-5-edition/chapter-5/problem-75-you-have-5-grams-of-carbon-14-whose-half-life-is-/

[8] https://brainly.in/question/9793176

[9] https://www.math.uni.edu/~campbell/mdm/cont.html

[10] https://www.comerica.com/insights/wealth-management/wealth-preservation/financially-fit-clients-do-math.html

[11] https://www.quora.com/How-long-will-it-take-to-double-your-savings-if-you-earn-5-percent-interest-compounded-annually

[12] https://prepp.in/question/at-what-percent-of-compound-interest-per-annum-a-s-65e1ec82d5a684356ea12319

I checked each and every of these references.

Part of them produced the treatment for precisely this posed problem, but all

produced treatments/answers were incorrect from the point of view of final rounding.

Other references were IRRELEVANT to the posed problem, which were especially sad to see.

Naturally, I informed Google AI Overview about this their mistake via their feedback system.

. . . . . . . . . . . . . . . . . . . .

In opposite, another Artificial Intelligence, https://math-gpt.org/, treats the problem IDEALLY (precisely as in my solution).

Question 729630: Bob, Ali and Glen went shopping. The total bill was $780.

If Ali and Glen bought the same amount and Bob hall as much as Ali and Glen,

How much did each person spend?

Explain answer.

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39792) (Show Source):

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Bob, Ali and Glen went shopping. The total bill was $780.

If Ali and Glen bought the same amount and Bob hall as much as Ali and Glen,

How much did each person spend?

Explain answer.

~~~~~~~~~~~~~~~~~~~~~~~

First you explain the question.

Question 729622: 1. formulate but DO NOT solve the problem.

the johnson farm has 600 acres of lad allotted for cultivating corn and wheat. the cost of cultivating corn and wheat (including seeds and labor) is $51 and $25/acre, respectively. Jacob Johnson has $20,200 available for cultivating these crops. if he wishes to use all the allotted land and his entire budget for cultivating these two crops, how many acres of each crop should he plant? Let X be the number of acres allotted for cultivating corn

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

1. formulate but DO NOT solve the problem.

the johnson farm has 600 acres of lad allotted for cultivating corn and wheat.

the cost of cultivating corn and wheat (including seeds and labor) is $51 and $25/acre, respectively.

Jacob Johnson has $20,200 available for cultivating these crops.

if he wishes to use all the allotted land and his entire budget for cultivating these two crops,

how many acres of each crop should he plant? Let X be the number of acres allotted for cultivating corn

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

I will strictly follow the instruction: "formulate but DO NOT solve".

X acres are for corn and 600-X acres are for wheat.

Write the money equation

51X + 25*(600-X) = 20200 dollars.

It is a single equation, which describes this problem.

And it is a single equation to solve.

Explained.

Question 729568: Calculate simple interest payable on a loan of $12000 borrowed from a bank at 15% per annum for 3 years

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Calculate simple interest payable on a loan of $12000 borrowed from a bank at 15% per annum for 3 years.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Use standard formula for the simple interest

I = 12000*3*0.15 = 5400 dollars. ANSWER

Solved.

------------------------------

The answer in the post by @lynnlo is incorrect, so ignore his post.

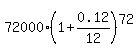

Question 729585: Principal amount is Rs.72000 and intrest is 12% and time period is 72 months take out compound intrest

Answer by ikleyn(53748) (Show Source):

You can put this solution on YOUR website! .

Principal amount is Rs.72000 and interest is 12% and time period is 72 months take out compound interest

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The compounding period is not given in the problem, which proves that the problem was created

by an amateur - not a professional Math writer.

I will assume that compounding is made monthly.

The future value is

FV =  = 147391.15 dollars.

The interest is the difference 147391.15 - 72000 = 77,391.15 dollars. ANSWER = 147391.15 dollars.

The interest is the difference 147391.15 - 72000 = 77,391.15 dollars. ANSWER

Solved.

|

Older solutions: 1..45, 46..90, 91..135, 136..180, 181..225, 226..270, 271..315, 316..360, 361..405, 406..450, 451..495, 496..540, 541..585, 586..630, 631..675, 676..720, 721..765, 766..810, 811..855, 856..900, 901..945, 946..990, 991..1035, 1036..1080, 1081..1125, 1126..1170, 1171..1215, 1216..1260, 1261..1305, 1306..1350, 1351..1395, 1396..1440, 1441..1485, 1486..1530, 1531..1575, 1576..1620, 1621..1665, 1666..1710, 1711..1755, 1756..1800, 1801..1845, 1846..1890, 1891..1935, 1936..1980, 1981..2025, 2026..2070, 2071..2115, 2116..2160, 2161..2205, 2206..2250, 2251..2295, 2296..2340, 2341..2385, 2386..2430, 2431..2475, 2476..2520, 2521..2565, 2566..2610, 2611..2655, 2656..2700, 2701..2745, 2746..2790, 2791..2835, 2836..2880, 2881..2925, 2926..2970, 2971..3015, 3016..3060, 3061..3105, 3106..3150, 3151..3195, 3196..3240, 3241..3285, 3286..3330, 3331..3375, 3376..3420, 3421..3465, 3466..3510, 3511..3555, 3556..3600, 3601..3645, 3646..3690, 3691..3735, 3736..3780, 3781..3825, 3826..3870, 3871..3915, 3916..3960, 3961..4005, 4006..4050, 4051..4095, 4096..4140, 4141..4185, 4186..4230, 4231..4275, 4276..4320, 4321..4365, 4366..4410, 4411..4455, 4456..4500, 4501..4545, 4546..4590, 4591..4635, 4636..4680, 4681..4725, 4726..4770, 4771..4815, 4816..4860, 4861..4905, 4906..4950, 4951..4995, 4996..5040, 5041..5085, 5086..5130, 5131..5175, 5176..5220, 5221..5265, 5266..5310, 5311..5355, 5356..5400, 5401..5445, 5446..5490, 5491..5535, 5536..5580, 5581..5625, 5626..5670, 5671..5715, 5716..5760, 5761..5805, 5806..5850, 5851..5895, 5896..5940, 5941..5985, 5986..6030, 6031..6075, 6076..6120, 6121..6165, 6166..6210, 6211..6255, 6256..6300, 6301..6345, 6346..6390, 6391..6435, 6436..6480, 6481..6525, 6526..6570, 6571..6615, 6616..6660, 6661..6705, 6706..6750, 6751..6795, 6796..6840, 6841..6885, 6886..6930, 6931..6975, 6976..7020, 7021..7065, 7066..7110, 7111..7155, 7156..7200, 7201..7245, 7246..7290, 7291..7335, 7336..7380, 7381..7425, 7426..7470, 7471..7515, 7516..7560, 7561..7605, 7606..7650, 7651..7695, 7696..7740, 7741..7785, 7786..7830, 7831..7875, 7876..7920, 7921..7965, 7966..8010, 8011..8055, 8056..8100, 8101..8145, 8146..8190, 8191..8235, 8236..8280, 8281..8325, 8326..8370, 8371..8415, 8416..8460, 8461..8505, 8506..8550, 8551..8595, 8596..8640, 8641..8685, 8686..8730, 8731..8775, 8776..8820, 8821..8865, 8866..8910, 8911..8955, 8956..9000, 9001..9045, 9046..9090, 9091..9135, 9136..9180, 9181..9225, 9226..9270, 9271..9315, 9316..9360, 9361..9405, 9406..9450, 9451..9495, 9496..9540, 9541..9585, 9586..9630, 9631..9675, 9676..9720, 9721..9765, 9766..9810, 9811..9855, 9856..9900, 9901..9945, 9946..9990, 9991..10035, 10036..10080, 10081..10125, 10126..10170, 10171..10215, 10216..10260, 10261..10305, 10306..10350, 10351..10395, 10396..10440, 10441..10485, 10486..10530, 10531..10575, 10576..10620, 10621..10665, 10666..10710, 10711..10755, 10756..10800, 10801..10845, 10846..10890, 10891..10935, 10936..10980, 10981..11025, 11026..11070, 11071..11115, 11116..11160, 11161..11205, 11206..11250, 11251..11295, 11296..11340, 11341..11385, 11386..11430, 11431..11475, 11476..11520, 11521..11565, 11566..11610, 11611..11655, 11656..11700, 11701..11745, 11746..11790, 11791..11835, 11836..11880, 11881..11925, 11926..11970, 11971..12015, 12016..12060, 12061..12105, 12106..12150, 12151..12195, 12196..12240, 12241..12285, 12286..12330, 12331..12375, 12376..12420, 12421..12465, 12466..12510, 12511..12555, 12556..12600, 12601..12645, 12646..12690, 12691..12735, 12736..12780, 12781..12825, 12826..12870, 12871..12915, 12916..12960, 12961..13005, 13006..13050, 13051..13095, 13096..13140, 13141..13185, 13186..13230, 13231..13275, 13276..13320, 13321..13365, 13366..13410, 13411..13455, 13456..13500, 13501..13545, 13546..13590, 13591..13635, 13636..13680, 13681..13725, 13726..13770, 13771..13815, 13816..13860, 13861..13905, 13906..13950, 13951..13995, 13996..14040, 14041..14085, 14086..14130, 14131..14175, 14176..14220, 14221..14265, 14266..14310, 14311..14355, 14356..14400, 14401..14445, 14446..14490, 14491..14535, 14536..14580, 14581..14625, 14626..14670, 14671..14715, 14716..14760, 14761..14805, 14806..14850, 14851..14895, 14896..14940, 14941..14985, 14986..15030, 15031..15075, 15076..15120, 15121..15165, 15166..15210, 15211..15255, 15256..15300, 15301..15345, 15346..15390, 15391..15435, 15436..15480, 15481..15525, 15526..15570, 15571..15615, 15616..15660, 15661..15705, 15706..15750, 15751..15795, 15796..15840, 15841..15885, 15886..15930, 15931..15975, 15976..16020, 16021..16065, 16066..16110, 16111..16155, 16156..16200, 16201..16245, 16246..16290, 16291..16335, 16336..16380, 16381..16425, 16426..16470, 16471..16515, 16516..16560, 16561..16605, 16606..16650, 16651..16695, 16696..16740, 16741..16785, 16786..16830, 16831..16875, 16876..16920, 16921..16965, 16966..17010, 17011..17055, 17056..17100, 17101..17145, 17146..17190, 17191..17235, 17236..17280, 17281..17325, 17326..17370, 17371..17415, 17416..17460, 17461..17505, 17506..17550, 17551..17595, 17596..17640, 17641..17685, 17686..17730, 17731..17775, 17776..17820, 17821..17865, 17866..17910, 17911..17955, 17956..18000, 18001..18045, 18046..18090, 18091..18135, 18136..18180, 18181..18225, 18226..18270, 18271..18315, 18316..18360, 18361..18405, 18406..18450, 18451..18495, 18496..18540, 18541..18585, 18586..18630, 18631..18675, 18676..18720

|