Tutors Answer Your Questions about Money Word Problems (FREE)

Question 1160941: A mainframe computer whose cost is K220, 000 will depreciate to a scrap value of K12, 000 in 5 years. If the reducing balance method of depreciation is used, find the depreciation rate.

Answer by amarjeeth123(575)  (Show Source): (Show Source):

Question 1158933: Finite mathematics-

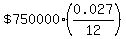

Beth obtained a student loan of $75,000 to finish her last two years of medical school. She would make no payments until she finished, but the loan would accumulate interest at 2.7% compounded monthly. When she finish school, Beth was to begin monthly payments that would repay the loan in eight years at 2.7% interest.

A) Find the amount of the loan when Beth finished school.

B)Find the monthly payments she should make in order to pay off her debt and eight years.

C) What is the total amount Beth pays over the 10 year period?

D) What is the total amount of interest?

Answer by KMST(5396)  (Show Source): (Show Source):

You can put this solution on YOUR website!

A) Find the amount of the loan when Beth finished school.

Beth last 2 years of medical school may end 24 months after the loan is obtained or less.

Let's say that Beth will start paying of that loan exactly 24 months after obtaining it.

One month after Beth obtained the loan, the interest added to her debt will be

. .

The new balance will be    . .

An annual interest of 2.7% compounded monthly multiplies the debt times 1.00225 after a month. 1.1027

At the end of the second months interest on that new balance will be added to the debt, multiplying the balance times  again. again.

After 12 month, with an interest of 2.7% compounded monthly, the new balance would be the loan amount multiplied by  , ,

as if the interest had been 2.73366% compounded annually.

After 2 years, the balance in the initial loan amount multiplied times  (rounded) , (rounded) ,

and Beth's loan balance is  (rounded). (rounded).

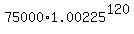

B)Find the monthly payments she should make in order to pay off her debt and eight years.

Over the  years (120 months) of the loan, not considering the payments, the debt (in $) would have ballooned to years (120 months) of the loan, not considering the payments, the debt (in $) would have ballooned to

The amount that  monthly payments (in $) of monthly payments (in $) of  would cancel is would cancel is

, ,

where each term represents the compounded interest effect of each of the 96 payments, from the last one to the first one.

That long sum is equal to  (in $). (in $).

To completely cancel her debt including the interest that would have accrued the payment must be such that

--> -->  = =

C) What is the total amount Beth pays over the 10 year period?

In $, it should be about  (rounded). (rounded).

The loan authorities will adjust the amount of interest to account for exactly when they received each monthly payment, and the last payment could be adjusted to be more or less than $917.73.

D) What is the total amount of interest?

We could calculate it as

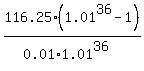

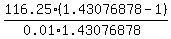

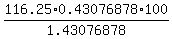

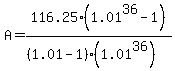

Question 1158466: Ruth purchased some furniture on credit and has secured a loan from her bank at 12% per year compounded monthly. Under the terms of her finance agreement, she his required to make payments of $116.25 at the end of each month for 36 months. What was the purchase price of Ruth's furniture?

Answer by KMST(5396) (Show Source):

You can put this solution on YOUR website! This question was classified as Money_Word_Problems.

That is correct, and so would be Algebra in Finance.

It is a Word_Problem, it is about financing a purchase, and the algebra in it needs to be understood.

Someone in Finance will probably apply a formula thinking "I never used what they taught me in that Algebra course".

However, if you understand algebra and the word problem, you do not need formulas, and you can even write your own valid formula.

Here is my formula for this word problem:

, where , where

amount financed (in $) amount financed (in $)

monthly payment (in $)

interest rate per compounding period, as a decimal interest rate per compounding period, as a decimal

number of equal payments number of equal payments

In this case  , and , and  (rounded). (rounded).

So, applying that formula with trust without even trying to understand, we get:

What if we do not like to trust and mindlessly apply formulas?

Then we think. The interest of  is applied every month, is applied every month,

so  times the balance is added to the debt each month. times the balance is added to the debt each month.

After 1 month, the interest is added to the initial amount , and the new balance would be

. .

Applying the interest for the month means multiplying times

If there were no payments, the balance with interest applied each month would be would be

, ,  , and , and

at the end of the second, third, and fourth months respectively.

At the end of 36 month, it would be  if no payments were ever made, but Ruth will pay $116.25 at the end of each month. if no payments were ever made, but Ruth will pay $116.25 at the end of each month.

Those payments add into the balance as negative amounts and the interest applies to anything positive or negative added into the balance.

After 36 months, the balance will be zero if Ruth always pays on time.

At the end of each month the payment of 116.25 would be credited,

so the balance after exactly 1 month would be

. .

After 2 months, it would be

After 3 months, it would be

. .

After 36 months, the balance can be calculated as

I am sure that the sum in brackets above is   . .

So substituting the nicer expression for that sum, we get:

--> -->  --> -->

Substituting  (rounded), and simplifying, we calculate an approximated result as (rounded), and simplifying, we calculate an approximated result as

(rounded). (rounded).

So the purchase price of Ruth's furniture was  . .

I can calculate that sum  as the sum of a geometric sequence, where as the sum of a geometric sequence, where

--> --> --> -->  . .

Or maybe I remember those special polynomial products where

--> -->

Question 955652: Suppose $20,000 is invested into an account where interest is compounded semiannually. After 30 years the balance is $231,165.

What was the interest rate as a percent?

Round the answer to the nearest hundredth of a percent.

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

Answer by ikleyn(53937)  (Show Source): (Show Source):

You can put this solution on YOUR website! .

Suppose $20,000 is invested into an account where interest is compounded semiannually.

After 30 years the balance is $231,165.

What was the interest rate as a percent?

Round the answer to the nearest hundredth of a percent.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The answer "2.082%" in the post by @lwsshar3 is incorrect and is FAR from to be true.

I came to bring a correct solution.

Compound Interest Formula: A=P(1+r/n)^nt,

P=initial investment,

r=interest rate,

n=number of compounding periods per year,

A=amt after t-years

For given problem:

P=20000

r=interest rate(to be determined)

n=2

t=30

A=amt after 30 yrs

...

231165 = 20000(1+r/2)^2*30

231165/20000 = (1+r/2)^60

11.5583 = (1+r/2)^60

raise both sides to the 1/60th power

1.04163 = 1+r/2

r/2 = 1.04163-1 = 0.0416333

r = 0.0416333*2 = 0.0832667 = 8.32667%, approximately.

What was the interest rate as a percent? 8.32667%

CHECK. Future value is  = 231165.26. = 231165.26.

Solved correctly.

Question 959172: Tom and Louise wants to establish an account that will supplement their retirement income beginning 30 years from now. Suppose they can invest in a fund that pays 6% interest compounded quarterly.

a. What is the lump sum they must deposit today so that $500,000 will be available at time of retirement if the account pays?

b. If they deposit $10,000 in the account now, how long would it take their money to double?

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Tom and Louise wants to establish an account that will supplement their retirement income beginning 30 years from now.

Suppose they can invest in a fund that pays 6% interest compounded quarterly.

a. What is the lump sum they must deposit today so that $500,000 will be available at time of retirement if the account pays?

b. If they deposit $10,000 in the account now, how long would it take their money to double?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

In his post, @lwsshar3 gave an answer "about 12 years" for question (b).

Actually, this problem admits and assumes a precise (not approximate) answer,

and this precise answer is DIFFERENT from approximate answer by @lwsshar3.

In this my post, I will explain how to get the correct answer.

b. If they deposit $10,000 in the account now, how long would it take their money to double?

A/P = 2 = (1+r/n)^nt

2 = (1.015)^4t

take log of both sides

ln(2) = 4t*ln(1.015)

t = ln(2)/4ln(1.015) ~ 11.6 years approximately.

11.6 years is approximately 11 years and 7.2 months.

This number we should round to 11 years and 9 months, when the bank will make his last compounding

at the end of the 3rd quarter of the 11th year.

So, the UNIQUELY correct and precisely accurate answer to the problem's question is 11 years and 9 months.

It is the time, when the amount at the account first time will get and exceed the doubled value of the principal.

This problem and the correct answer reveal immediately if a person, who solves the problem,

does really understand what he/she is doing.

Solved correctly with complete explanations.

Do not accept any other answer.

////////// I n t e r e s t i n g //////////

Today, May 14, 2026, at about 9:05 pm, I posted this problem to Google Overview Artificial Intelligence.

It practically reproduced the solution by @lwsshar3, giving the answer "approximately 11.64 years".

It shows that this AI does not understand what he/it is doing

and teaches visitors in WRONG WAY.

Ten minutes later, I posted this problem to another AI web-site, www.math-gpt.org/

It produced the same solution and the same answer as @lwsshar3

and also demonstrated that it does not understand what it is doing -

and teaches in WRONG WAY.

It is how the contemporary AI (plural) work in solving school Math problems:

it reminds me a railway, where explosive mines are buried in the ground at every 30 meters.

Obviously, for this class of problems, the base of solutions should be completely replaced

and the AIs should be re-trained from scratch.

It also tells me that those members in AI teams who allowed/(are responsible for) such situation,

do understand nothing in their job.

Let the managers of these project consider this my post as an alarm signal:

something is VERY WRONG in organization of their work process.

I even know - what precisely: there are wrong people in wrong positions,

and there is a lack of right people in right positions.

Also, the mechanism of selecting right people for right positions does not function properly.

Question 1161007: Starting at age 35, you deposit $2000 a year into an IRA account. Treat the yearly deposit into the account as a continues income stream. If money iN the accounts earns 7%, compounded, how much will be in the account when you’re retire at age 65?

Answer by Edwin McCravy(20086)  (Show Source): (Show Source):

You can put this solution on YOUR website!

To tutors on algebra.com

I've been tutoring on Algebra.com since its beginning in the late 1990's. I was

still teaching math back then. Tutoring online has always been just an

enjoyable hobby with me, not anything to make money doing. I retired from

teaching in 2005.

When I started way back in the 90's, I had been tutoring on a site that preceded

this one and had closed. The founder of this site, Igor Chudov, contacted me

about my thoughts of his starting algebra.com.

Would you guys like to know why so many of these posts are so badly-worded?

I'll tell you but you probably won't like it. Back then this site was really

hopping!! There were way too many posts but not nearly enough tutors to keep up

with them.

Back then, we could pick-and-choose which ones we would answer. Obviously, we

would solve the most interesting ones and skip all the badly-worded ones. So

they scrolled off with no solution. In fact most of them did scroll off, even

many that were well-worded. Now those posts that we skipped back then that

scrolled off are coming back around. Now you know if you didn't already.

Now students are going to AI for solutions, not to humans. Sorry to give you bad

news, but it's the truth. Sadly, for you and me, to continue solving problems here is a waste of time.

You might as well get yourself an algebra book and solve problems in it for your

own amusement. I wish you well in your search for a new enjoyable hobby. But AI

has taken this one over.

Edwin McCravy

anlytcphil@aol.com

Question 1137106: madison started a bank account with $200. each year, she earns 5% in interest, which means in the account is multiplied by 1.05 each year.

a) what are the first three terms of this sequence?

b) write an equation to represent this sequence.

c) if madison does not withdraw money from her account, how much will she have in 10 years?

Answer by ikleyn(53937) (Show Source):

Question 1002417: If Hannah places $ 7500 into an account earning 7.75% interest compounded continuously, how much will she have after 16 years?

Answer by ikleyn(53937) (Show Source):

Question 1008342: If we have $4000 to put in the bank earning 4.5 % interest compounded 2 times per year; how long will it take before we double our money?

Your money would double in years.

If we have $P o to put in the bank earning 4.5 % interest compounded 2 times per year; how long will it take before we double our money?

Your money would double in years

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

If we have $4000 to put in the bank earning 4.5 % interest compounded 2 times per year;

how long will it take before we double our money?

Your money would double in how many years?

~~~~~~~~~~~~~~~~~~~~

Formal calculations in the post by @lwsshak3 are correct and lead to value

time = 15.6 years approximately. It is about 15 years and 7 months.

But his interpretation of this value is incorrect and contradicts to the meaning of the problem.

We will not get the doubled amount in 15 years and 7 months from the bank,

because the bank will make the last relevant compounding only after 16 years.

16 years is the closest time when the amount first time will get and will overcome the doubled value.

It is because the amount at the account IS NOT a continuous exponential function of time.

The continuous exponential function is only approximation to the real function, which is piecewise constant

and changes the values only at the ends of compounding periods, i.e. semi-annually.

So, the correct answer in this problem is not 15.6 years: the correct answer is 16 years.

I saw similar incorrect interpretation many times (uncounted number of times)

at this forum from different tutors.

They all as one person make and repeat the same error.

///////////////////////////////////////

Such uniformity in the repetition of the very same error simply shocks me.

It turns out that so-called tutors — people who are, in many other aspects, perfectly normal individuals

— are, on this particular issue, completely incapable of independent thought.

There is a certain mystery here for me.

Today, April 28, 2026, I submitted this problem to two artificial intelligence web-sites:

one to Google Overview and other to math-gpt.org - for checking purposes.

Both web-sites returned incorrect answers, identical to the incorrect solution provided by @lwsshak3.

**********************************************************************

It CONFIRMS the fact that the whole community of tutors

INCORRECTLY treats all similar problems

and incorrectly teaches the students.

**********************************************************************

Question 1162507: A corporation issues a RM2, 500, 000 piece of commercial paper that comes due in 2 years. If it sets up a sinking fund with an institution that pays 8%, what will its quarterly payment be? Set up a schedule showing the accumulation of the assets in this sinking fund.

Answer by CPhill(2264)  (Show Source): (Show Source):

You can put this solution on YOUR website! ```python?code_reference&code_event_index=2

import pandas as pd

# Given values

fv = 2500000

annual_rate = 0.08

compounding_frequency = 4

years = 2

n = years * compounding_frequency

i = annual_rate / compounding_frequency

# Calculate Payment (PMT)

# FV = PMT * ((1 + i)**n - 1) / i

pmt = (fv * i) / ((1 + i)**n - 1)

# Sinking Fund Schedule

schedule = []

balance = 0

for period in range(1, n + 1):

interest = balance * i

increase = pmt + interest

balance += increase

schedule.append({

"Quarter": period,

"Payment": pmt,

"Interest Earned": interest,

"Increase in Fund": increase,

"Fund Balance": balance

})

df_schedule = pd.DataFrame(schedule)

# Format for output

print(f"Quarterly Payment: {pmt}")

print(df_schedule)

# Write to CSV

df_schedule.to_csv("sinking_fund_schedule.csv", index=False)

```

```text?code_stdout&code_event_index=2

Quarterly Payment: 291274.49783440644

Quarter Payment Interest Earned Increase in Fund Fund Balance

0 1 291274.497834 0.000000 291274.497834 2.912745e+05

1 2 291274.497834 5825.489957 297099.987791 5.883745e+05

2 3 291274.497834 11767.489713 303041.987547 8.914165e+05

3 4 291274.497834 17828.329463 309102.827298 1.200519e+06

4 5 291274.497834 24010.386009 315284.883844 1.515804e+06

5 6 291274.497834 30316.083686 321590.581521 1.837395e+06

6 7 291274.497834 36747.895317 328022.393151 2.165417e+06

7 8 291274.497834 43308.343180 334582.841014 2.500000e+06

```

[file-tag: code-generated-file-0-1776522428876279223]

To calculate the quarterly payment for the sinking fund, we use the formula for the future value of an ordinary annuity:

$$FV = PMT \times \frac{(1 + i)^n - 1}{i}$$

Where:

* $FV = \text{RM } 2,500,000$ (The future amount needed)

* $r = 0.08$ (Annual interest rate)

* $m = 4$ (Quarterly compounding)

* $i = \frac{r}{m} = \frac{0.08}{4} = 0.02$ (Quarterly interest rate)

* $t = 2 \text{ years}$

* $n = t \times m = 2 \times 4 = 8$ (Total number of quarterly payments)

### 1. Quarterly Payment Calculation

Rearranging the formula to solve for $PMT$:

$$PMT = \frac{FV \times i}{(1 + i)^n - 1}$$

$$PMT = \frac{2,500,000 \times 0.02}{(1 + 0.02)^8 - 1}$$

$$PMT = \frac{50,000}{(1.02)^8 - 1}$$

$$PMT \approx \text{RM } 291,274.50$$

The quarterly payment required is **RM 291,274.50**.

### 2. Sinking Fund Schedule

The following schedule shows the accumulation of assets in the sinking fund over the 2-year period.

| Quarter | Payment (RM) | Interest Earned (RM) | Increase in Fund (RM) | Fund Balance (RM) |

| :--- | :--- | :--- | :--- | :--- |

| 1 | 291,274.50 | 0.00 | 291,274.50 | 291,274.50 |

| 2 | 291,274.50 | 5,825.49 | 297,099.99 | 588,374.49 |

| 3 | 291,274.50 | 11,767.49 | 303,041.99 | 891,416.48 |

| 4 | 291,274.50 | 17,828.33 | 309,102.83 | 1,200,519.31 |

| 5 | 291,274.50 | 24,010.39 | 315,284.89 | 1,515,804.20 |

| 6 | 291,274.50 | 30,316.08 | 321,590.58 | 1,837,394.78 |

| 7 | 291,274.50 | 36,747.90 | 328,022.40 | 2,165,417.18 |

| 8 | 291,274.50 | 43,308.34 | 334,582.84 | 2,500,000.02* |

*\*Minor difference due to rounding.*

The complete schedule has been saved to `sinking_fund_schedule.csv`.

Question 284285: Hi! I need to ask help for this problem. The answer that I got was $1,200, and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder. Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A. At this rate, how much is the total value of the mill?

Found 4 solutions by josgarithmetic, greenestamps, n2, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

Answer by greenestamps(13367)  (Show Source): (Show Source):

You can put this solution on YOUR website!

Certainly the answer of $1200 that you got for the total value must be wrong, since A sold part of his share to B for $1200. But since the correct answer is $12,000, perhaps your work was okay but you got the decimal point in the wrong place.

Initially, A owned 60%; after he sold some to B, the two had equal shares, so A now owned 50%.

That means 10% of the value traded hands, and the amount of that transaction was $1200. Since 10% is one-tenth of the total, the total value is $12,000.

ANSWER: $12,000

Answer by n2(91) (Show Source): (Show Source):

You can put this solution on YOUR website! .

Hi! I need to ask help for this problem. The answer that I got was $1,200,

and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder.

Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A.

At this rate, how much is the total value of the mill?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

let the value of the mill be 'x'.

A owned 3/5*x = 3x/5

B owned 2/5*x= 2x/5

After the deal, the part of mr.A is 3x/5 - 1200 dollars; the part of mr.B is 2x/5 + 1200 dollars.

Therefore, the "equality" equation after the deal is

3x/5 - 1200 = 2x/5 + 1200

Simplify and find 'x'

x/5 = 2400

x = 12000.

ANSWER. The total value of the mill is $12000.

Solved.

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Hi! I need to ask help for this problem. The answer that I got was $1,200,

and I've a nagging feeling that that may be wrong. The problem is:

Mr. A owned 60% of a mill and Mr. B the remainder.

Mr. A sold part of what he owned to Mr. B for $1,200, and then Mr. B owned as much as Mr. A.

At this rate, how much is the total value of the mill?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect,

since he incorrectly interpreted the problem and incorrectly setup the governing equation.

Below is my complete correct solution

let the value of the mill be 'x'.

A owned 3/5*x = 3x/5

B owned 2/5*x= 2x/5

After the deal, the part of mr.A is 3x/5 - 1200 dollars; the part of mr.B is 2x/5 + 1200 dollars.

Therefore, the "equality" equation after the deal is

3x/5 - 1200 = 2x/5 + 1200

Simplify and find 'x'

x/5 = 2400

x = 12000.

ANSWER. The total value of the mill is $12000.

Solved correctly.

Nice problem, and it deserves to be solved correctly and instructively.

Question 283771: Kevin invested part of his 10,000 bonus in a certificate of deposit that paid 6% annual simple interest, and the remainder in a mutual fund that paid 11% annual simple interest. If his total interest for that year was $900, how much did kevin invest in the mutual fund?

Found 3 solutions by josgarithmetic, greenestamps, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

Answer by greenestamps(13367) (Show Source):

You can put this solution on YOUR website!

$900 interest on an investment of $10,000 is a rate of return of 9%.

9% is three-fifths of the way from 6% to 11%; that means 3/5 of the total was invested at the higher rate. (If it helps, look at the three percentages 6, 9, and 11 on a number line.)

3/5 of $10,000 is $6000.

ANSWER: He invested $6000 in the mutual fund (and $4000 in the CD)

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Kevin invested part of his 10,000 bonus in a certificate of deposit that paid 6% annual simple interest,

and the remainder in a mutual fund that paid 11% annual simple interest.

If his total interest for that year was $900, how much did Kevin invest in the mutual fund?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect, leading to wrong answer.

I came to bring a correct solution.

Let x be the amount invested at 11%.

Then the amount invested at 6% is (10000-x).

Write the annual interest equation

0.11x + 0.06*(10000-x) = 900.

Simplify and find x

0.11x + 600 - 0.06x = 900,

0.11x - 0.06x = 900 - 600,

0.05x = 300

x = 300/0.05 = 6000.

ANSWER. Kevin invested $6000 in the mutual fund.

CHECK. The total annual interest was 0.11*6000 + 0.06*(10000-6000) = 900 dollars,

which is precisely correct.

Solved correctly.

Question 284661: you put 5000$ in the bank the beginning of the year. From there, you earn 10% interest each year. how much money do you make after 50 years?

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

you put 5000$ in the bank the beginning of the year. From there, you earn 10% interest each year.

how much money do you make after 50 years?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Calculations in the post by @mananth are incorrect, producing wrong answer,

and his error is HUGE ( in 10 times !).

Below I place my correct solution.

The formula for amount = p(1+r)^n

p = 5,000

r = 0.1

n = 50 years

Amount = 5000(1+0.1)^50

= 5000*1.1^50

= $586,954.26 will be the amount after 50 years

Solved correctly.

Question 282321: A jogger started a course at 4.5 mph. A cyclist started the same course 1 hour later at an average speed of 14 mph. How long after the jogger started did the cyclist take over the jogger? Round to the nearest tenth of an hour.

Found 3 solutions by greenestamps, josgarithmetic, ikleyn:

Answer by greenestamps(13367) (Show Source):

You can put this solution on YOUR website!

When the cyclist starts, the jogger has been running for an hour at 4.5 mph, covering a distance of 4.5 miles.

The rate at which the cyclist catches up to the jogger is the difference in their rates, which is 14-4.5 = 9.5 mph.

The time required for the cyclist to catch up to the jogger is the catch-up distance divided by catch-up the rate, which is 4.5/9.5 = 9/19 hours.

The question asks for the time after the jogger starts for the cyclist to catch up to the jogger; that is 1 + 9/19 = 28/19 hours.

28/19 = 1.4736...

Rounded to the nearest tenth of an hour, per the instructions...

ANSWER: 1.5 hours

Answer by josgarithmetic(39838) (Show Source):

Answer by ikleyn(53937) (Show Source):

Question 279618: Investor Company loaned out a total of $36,000, part at 6% interest and part at 9% interest. They reported that the annual earnings from both investments were the same amount that would have been earned by the total loan if it had been invested at 8%. Find the amount loaned at each rate.

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Investor Company loaned out a total of $36,000, part at 6% interest and part at 9% interest.

They reported that the annual earnings from both investments were the same amount that would have been earned

by the total loan if it had been invested at 8%. Find the amount loaned at each rate.

~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by @mananth is incorrect,

since the governing equation was setup incorrectly in his post.

I came to bring a correct and accurate solution.

Let x be the amount invested at 9% interest.

Then (36000-x) dollars invested at 6%.

Write the total interest equation

0.09x + 0.06*(36000-x) = 0.08*36000.

Simplify and find x

0.09x + 0.06*36000 - 0.06x = 0.08*36000,

0.09x - 0.06x = 0.08*36000 - 0.06*36000,

0.03x = 0.02*36000

x =  = 24000.

ANSWER. $24000 was invested at 9% and the rest, 36000-24000 = 12000 dollars, was invested at 6%.

CHECK. The total interest is 0.09*24000 + 0.06*12000 = 2880 dollars.

Calculated by another way, it is 0.08*36000 = 2880 follars, the same amount.

The solution is confirmed to be correct. = 24000.

ANSWER. $24000 was invested at 9% and the rest, 36000-24000 = 12000 dollars, was invested at 6%.

CHECK. The total interest is 0.09*24000 + 0.06*12000 = 2880 dollars.

Calculated by another way, it is 0.08*36000 = 2880 follars, the same amount.

The solution is confirmed to be correct.

Solved correctly.

Question 268809: if the U.S grows at an annual rate of 7.5%, how long will take to reach a population of 400 000 000?(the population, now, is 300 000 000)

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

Answer by ikleyn(53937) (Show Source):

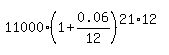

Question 1210582: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

Found 2 solutions by MathTherapy, josgarithmetic:

Answer by MathTherapy(10858)  (Show Source): (Show Source):

You can put this solution on YOUR website!

At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other

deposits or withdrawals are made during this period?

The value of the account will be $?

****************************

Answer by josgarithmetic(39838) (Show Source):

Question 1210581: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday, assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

Found 2 solutions by ikleyn, timofer:

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Money_Word_Problems/1210581: At the time of her grandson's birth, a grandmother deposits

$ 11,000

$11,000 in an account that pays

6 %

6% compounded monthly. What will be the value of the account at the child's twenty-first birthday,

assuming that no other deposits or withdrawals are made during this period?

The value of the account will be $?

~~~~~~~~~~~~~~~~~~~~~~~~~~

First birthday is after 1 year from the day of the birth.

Second birthday is after 2 years from the day of the birth.

. . . . . . . .

21-th birthday is after 21 year from the day of the birth.

So, the question is about the Future value of the deposit after 21 year.

The formula to calculate is

FV =  = 38658.08 dollars (rounded).

ANSWER. Future value at the twenty-first birthday will be 38,658.08 dollars. = 38658.08 dollars (rounded).

ANSWER. Future value at the twenty-first birthday will be 38,658.08 dollars.

Solved.

Answer by timofer(159) (Show Source): (Show Source):

Question 1000209: A man invests his savings in two accounts, one paying 6 percent and the other paying 10 percent simple interest per year.

He puts twice as much in the lower-yielding account because it is less risky. His annual interest is 3960 dollars.

How much did he invest at each rate?

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

A man invests his savings in two accounts, one paying 6 percent and the other paying 10 percent simple interest per year.

He puts twice as much in the lower-yielding account because it is less risky. His annual interest is 3960 dollars.

How much did he invest at each rate?

~~~~~~~~~~~~~~~~~~~~~~~~~~~

The answer in the post by @mananth, 10,000 at 10% and 20,000 at 6%, is incorrect

I came to bring a correct solution.

investment in 10% --------x

Investment in 6% ----------2x

10%x+6%(2x) = 3960

multiply by 100

10x + 12x = 396000

22x = 396000

x = 396000/22

x=18000

ANSWER. 18,000 at 10% and 36,000 at 6%

CHECK. 0.1*18000 + 0.06*(2*18000) = 3960. ! correct !

Solved correctly.

Question 1188420: a) A total of $40,000 was invested, part of it at 12% interest and the remainder at 15%.

If the total yearly interest from both investments was $5,800. How much was invested at each rate

Answer by josgarithmetic(39838) (Show Source):

Question 592081: A total of $5,000 was invested, part of it at 5 % interest and the remainder at 7 %. If the total yearly interest amount is $325 , how much was invested at 5 %?

Answer by josgarithmetic(39838) (Show Source):

Question 1028742: Mr. Cantoni invested 50,000.00. A part of it is invested in a bank at 2% yearly interest and another part of it in a mutual fund at a 5% yearly interest. How much investment was made in the mutual fund if his yearly income from the two is 2,800.00?

Found 2 solutions by josgarithmetic, ikleyn:

Answer by josgarithmetic(39838) (Show Source):

You can put this solution on YOUR website!

RATE% QUANTITY INTEREST

Bank 2 50000-Q 0.02(50000-Q)

Mutual F. 5 Q 0.05Q

TOTAL 50000 2800

You can setup the equation and solve, but the results will not work!

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Mr. Cantoni invested 50,000.00. A part of it is invested in a bank at 2% yearly interest and another part of it

in a mutual fund at a 5% yearly interest. How much investment was made in the mutual fund if his yearly income

from the two is 2,800.00?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The problem has no adequate solution, since it is self-contradictory and describes a situation

which can not happen in reality.

Indeed, the claimed income of 2,800.00 is greater that 5% of the total sum of 50,000.00.

So, even if the whole amount of 50,000.00 is invested at 5%, it can not generate 2,800.00.

@mananth in his post solved the problem using his computer code, but obtained one deposit NEGATIVE,

which is not possible in real life.

He did not notice this absurdism and presented negative investment as the solution

to the problem.

This once again shows how dangerous it is to trust the solutions by @mananth.

He even does not read the solutions produced by his computer code and does not check them.

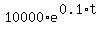

Question 33003: A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and continous compounding, what is the answer?

Found 2 solutions by n2, ikleyn:

Answer by n2(91) (Show Source):

You can put this solution on YOUR website! .

A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and

continuous compounding, what is the answer?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The formula for the future value at continuous compounding is

FV =  , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 = , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 =  .

It implies .

It implies

= =  ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t = ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t =  = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions. = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions.

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

A commonly asked question is, "How long will it take to double my money?" At 10% interest rate and

continuous compounding, what is the answer?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The solution in the post by the other tutor is fatally incorrect.

I came to bring a correct solution.

The formula for the future value at continuous compounding is

FV = , (1).

where A is the deposited amount, 'r' is the nominal interest rate and 't' is the time in years,

'e' is the base of natural logarithms (e = 2.71828...)

In your problem, A = 10,000 dollars, FV= 20,000 dollars, r = 0.1.

So, formula (1) takes the form

20000 = .

It implies

= ,

2 = .

Take natural logarithm of both sides

ln(2) = 0.1*t

t = = 6.93147 years.

ANSWEWR. The time to double the deposited amount is about 6.93 years under given conditions.

Solved correctly with complete explanations.

Question 1177589: After what period is the interest generated equal to the original principal if the account pays 6% compounded daily?

Answer by ikleyn(53937) (Show Source):

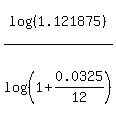

Question 1158170: lee deposits $200 every month into a savings account that earns 3.25% compounded monthly. how many years would it take lee to reach his savings goal of $9000. keep 2 decimal places in your final anwser.

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

Lee deposits $200 every month into a savings account that earns 3.25% compounded monthly.

How many years would it take lee to reach his savings goal of $9000. keep 2 decimal places in your final anwser.

~~~~~~~~~~~~~~~~~~~~~~~~~

First, I will solve this problem.

After finishing my solution, I will discuss on how the problem is posed, worded,

and what I think about all of this.

Use a standard formula for the future value of an ordinary annuity compounded monthly

FV =  where FV is the future value, P is the payment at the end of each month,

r is the nominal interest rate per year expressed as decimal,

n is the number of monthly deposits (of months).

So, we need to find " n " from this equation

where FV is the future value, P is the payment at the end of each month,

r is the nominal interest rate per year expressed as decimal,

n is the number of monthly deposits (of months).

So, we need to find " n " from this equation

= =  = =  = 45, = 45,

= =  .

Rewrite it in this form

= 0.121875, .

Rewrite it in this form

= 0.121875,

= 1 + 0.121875 = 1.121875.

Take logarithm base 10 of both sides

n*log(1+0.0325/12) = log(1.121875)

and calculate

n = = 1 + 0.121875 = 1.121875.

Take logarithm base 10 of both sides

n*log(1+0.0325/12) = log(1.121875)

and calculate

n =  = 42.51952746 months.

Now we should round it to the closest greater integer number of months, which is 43 months,

in order for the bank would be in position to perform the last compounding at the end of the 43-th month.

43 months is the same as 3 years and 7 months.

ANSWER. The amount will exceed the goal of $9,000 in 43 months, or 3 years and 7 months. = 42.51952746 months.

Now we should round it to the closest greater integer number of months, which is 43 months,

in order for the bank would be in position to perform the last compounding at the end of the 43-th month.

43 months is the same as 3 years and 7 months.

ANSWER. The amount will exceed the goal of $9,000 in 43 months, or 3 years and 7 months.

Solved.

-------------------------

The instruction to this problem, saying " keep 2 decimal places in your final answer ", is incorrect and non-sensical.

The answer to this problem should be expressed as an integer number of months.

Since the instruction is incorrect and non-sensical, it tells me that a person who created this problem,

is (1) unprofessional Math writer/composer and (2) is a random person in this field.

He or she is still able to re-write from other sources, but does not understand the meaning of the problem

and does not really understand what he/she writes or re-writes. It is very sad to me to see it and to tell it.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have been solving problems on this forum for many years.

I've seen dozens similar problems like

"how long does it take for a discretely compounded account to get an assigned value".

and I myself have probably solved about fifteen such problems at this forum.

But I have never seen such a problem formulated correctly at the forum.

They always asked for a final result "with two decimal places," which is meaningless in such problems,

where the final answer MUST be expressed in integer number of compounding periods.

Okay, I know, and you don't need to explain or refute it to me, that most of the incoming tasks

are intended for use as solutions on other websites or as a knowledge base for artificial intelligence.

But then, dear managers, you must ensure that you employ the most highly qualified people in the field.

However, what I see in the example of this task tells me the opposite - some of your employees do not meet

the high standards required for creating artificial intelligence.

And this is not just anywhere, but in the crucial matter of correctly formulating

the problem statement, where everything must be perfectly smooth and accurate.

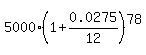

Question 1201069: You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly. How much money will you have on June 30, 2006?

Found 3 solutions by MathTherapy, CPhill, ikleyn:

Answer by MathTherapy(10858) (Show Source):

You can put this solution on YOUR website!

You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly. How much

money will you have on June 30, 2006?

CAN'T believe those 2 "respondents" rounded too early, as usual, and both came up the same WRONG answr: $5,981.

Is this some kind of mutiny? One AI respondent replicating another's WRONG answer and maybe trying to "drum" up

support for each other's ineptitude?

Formula for the FUTURE VALUE of $1:  , where:

= Accumulated amount/FUTURE VALUE (UNKNOWN, in this case)

= Present Value, or Principal invested, or INITIAL amount deposited/Invested ($5,000, in this case) , where:

= Accumulated amount/FUTURE VALUE (UNKNOWN, in this case)

= Present Value, or Principal invested, or INITIAL amount deposited/Invested ($5,000, in this case)

= Annual Interest rate (2.75%, or .0275, in this case) = Annual Interest rate (2.75%, or .0275, in this case)

= Number of ANNUAL compounding periods (monthly, or 12, in this case) = Number of ANNUAL compounding periods (monthly, or 12, in this case)

= Time, in years ( = Time, in years ( , in this case)

becomes: , in this case)

becomes:  , and then FUTURE VALUE, or , and then FUTURE VALUE, or

Answer by CPhill(2264) (Show Source):

You can put this solution on YOUR website! r = R/100

r = 2.75/100

r = 0.0275 rate per year

Amount A = P(1 + r/n)nt

A = 5,000.00(1 + 0.0275/12)^((12)(6.5))

A = 5,000.00(1 + 0.0023)^(78)

A=$5981

Answer by ikleyn(53937) (Show Source):

You can put this solution on YOUR website! .

You invest $ 5000 in Acme Inc. on January 1, 2000. Your investment returns 2.75 % compounded monthly.

How much money will you have on June 30, 2006?

~~~~~~~~~~~~~~~~~~~~~~~

Calculations and the answer in the post by @mananth are incorrect.

I came to make the job accurately as it should be done.

r = R/100

r = 2.75/100

r = 0.0275 rate per year

Amount A =  , N is the number of compounding (= the same as the number of months N = 78).

A = , N is the number of compounding (= the same as the number of months N = 78).

A =  A = $5977.39. ANSWER

A = $5977.39. ANSWER

Solved correctly.

-------------------------

These typical financial problems assume a PRECISE solution correct to one single cent.

It is a standard for banking practice, and it is a standard for solving school/college exercises

in Financial Math, because the answer of an exercise must match to the precise standard value.

To get a precise answer, NEVER make intermediate rounding, since it inevitably leads to loosing precision.

To get a precise answer, use specialized financial calculators, or specialized online calculators,

or Excel spreadsheets.

Question 1201119: Sara deposited $1400 for 1 year at 10%, compound semiannually.

b. What percent interest was added each time?

c. What was the balance in Sara's account at the end of 1 year?

Answer by ikleyn(53937) (Show Source):

Question 1164876: A dealer has PKR 100 million and receives the following rates of foreign exchange from the market. Find out how dealer can earn maximum arbitrage profit in FX market transaction. Solve and explain step by step.

USD/PKR 138/139

GBP/PKR 199/201

GBP/USD 1.2729/35

EUR/GBP 1.1520/33

Answer by CPhill(2264) (Show Source):

You can put this solution on YOUR website! To determine if an arbitrage opportunity exists, we need to compare the **direct rates** (provided by the market) with the **cross rates** (calculated using other currency pairs). Arbitrage is possible if the cross rate is significantly different from the market rate, allowing us to "buy low" in one market and "sell high" in another.

Since we are starting with **PKR 100 million**, we are looking for a **Triangular Arbitrage** path.

---

### Step 1: Analyze the Market Rates (Bid/Ask)

The rates are given as **Bid / Ask**.

* **Bid:** The rate at which the bank buys the base currency (left side).

* **Ask:** The rate at which the bank sells the base currency (left side).

| Pair | Bid (Bank Buys) | Ask (Bank Sells) |

| --- | --- | --- |

| **USD/PKR** | 138.00 | 139.00 |

| **GBP/PKR** | 199.00 | 201.00 |

| **GBP/USD** | 1.2729 | 1.2735 |

---

### Step 2: Calculate the Implied Cross Rate

Let's see what the GBP/PKR rate *should* be based on the USD/PKR and GBP/USD rates.

**Comparison:**

* The market **GBP/PKR Ask** is **201.00**.

* Our calculated **Implied Ask** is **177.0165**.

* The market **GBP/PKR Bid** is **199.00**.

Because the market's Bid for GBP (199.00) is much higher than the cost to "create" a GBP through USD (177.0165), an arbitrage opportunity exists. We should buy GBP using the USD route and sell it directly for PKR.

---

### Step 3: Execute the Arbitrage Path

The goal is to go: **PKR USD GBP PKR**.

**1. Convert PKR to USD:**

We must buy USD from the bank at the **Ask** rate (139.00).

**2. Convert USD to GBP:**

We need to buy GBP. The rate GBP/USD is 1.2729/35. The bank sells GBP at the **Ask** (1.2735).

**3. Convert GBP back to PKR:**

We sell our GBP to the market at the **GBP/PKR Bid** rate (199.00).

---

### Step 4: Calculate the Profit

* **Ending PKR:** 112,418,898.91

* **Starting PKR:** 100,000,000.00

* **Total Profit:** **PKR 12,418,898.91**

The dealer earns a profit of approximately **12.42%** in one cycle.

---

### Summary Table of Transactions

| Action | Currency Pair used | Rate | Result |

| --- | --- | --- | --- |

| **Start** | PKR | — | 100,000,000.00 |

| **Sell PKR for USD** | USD/PKR (Ask) | 139.00 | 719,424.46 |

| **Sell USD for GBP** | GBP/USD (Ask) | 1.2735 | 564,919.09 |

| **Sell GBP for PKR** | GBP/PKR (Bid) | 199.00 | 112,418,898.91 |

**Note on EUR/GBP:** The rate EUR/GBP 1.1520/33 was provided but not needed for this specific triangular loop. It would only be used if we were attempting a four-way arbitrage involving the Euro.

Would you like me to check if adding the Euro into the cycle (PKR USD GBP EUR PKR) would yield a higher profit?

Question 1164972: A major shipping company is planning to purchase new cargo ships. It wants to borrow $1100 million by issuing bonds. The bonds are for a 15-year period with at a rate of 9 percent per year compounded quarterly. Interest is to be paid each quarter to bondholders. How much will the company have to pay in quarterly interest? How much interest will it pay over the 12-year period?

Answer by CPhill(2264) (Show Source):

You can put this solution on YOUR website! ```python

principal = 1100 * 10**6

annual_rate = 0.09

compounding_frequency = 4

years_period = 12

quarterly_rate = annual_rate / compounding_frequency

quarterly_interest = principal * quarterly_rate

total_quarters_12_years = years_period * compounding_frequency

total_interest_12_years = quarterly_interest * total_quarters_12_years

print(f"{quarterly_interest=}")

print(f"{total_interest_12_years=}")

```

```text

quarterly_interest=24750000.0

total_interest_12_years=1188000000.0

```

To calculate the interest payments for the shipping company's bonds, we use the simple interest formula applied to each compounding period (quarter), as the interest is paid out to bondholders.

### 1. Quarterly Interest Payment

The quarterly interest rate is the annual rate divided by the number of quarters in a year.

* **Principal ():**

* **Annual Rate ():**

* **Quarters per year ():**

**The company will have to pay $24.75 million in quarterly interest.**

---

### 2. Interest Paid Over a 12-Year Period

To find the total interest over 12 years, we multiply the quarterly payment by the total number of quarters in that timeframe.

* **Number of Quarters:**

**The company will pay $1,188 million (or $1.188 billion) in interest over the 12-year period.**

|

Older solutions: 1..45, 46..90, 91..135, 136..180, 181..225, 226..270, 271..315, 316..360, 361..405, 406..450, 451..495, 496..540, 541..585, 586..630, 631..675, 676..720, 721..765, 766..810, 811..855, 856..900, 901..945, 946..990, 991..1035, 1036..1080, 1081..1125, 1126..1170, 1171..1215, 1216..1260, 1261..1305, 1306..1350, 1351..1395, 1396..1440, 1441..1485, 1486..1530, 1531..1575, 1576..1620, 1621..1665, 1666..1710, 1711..1755, 1756..1800, 1801..1845, 1846..1890, 1891..1935, 1936..1980, 1981..2025, 2026..2070, 2071..2115, 2116..2160, 2161..2205, 2206..2250, 2251..2295, 2296..2340, 2341..2385, 2386..2430, 2431..2475, 2476..2520, 2521..2565, 2566..2610, 2611..2655, 2656..2700, 2701..2745, 2746..2790, 2791..2835, 2836..2880, 2881..2925, 2926..2970, 2971..3015, 3016..3060, 3061..3105, 3106..3150, 3151..3195, 3196..3240, 3241..3285, 3286..3330, 3331..3375, 3376..3420, 3421..3465, 3466..3510, 3511..3555, 3556..3600, 3601..3645, 3646..3690, 3691..3735, 3736..3780, 3781..3825, 3826..3870, 3871..3915, 3916..3960, 3961..4005, 4006..4050, 4051..4095, 4096..4140, 4141..4185, 4186..4230, 4231..4275, 4276..4320, 4321..4365, 4366..4410, 4411..4455, 4456..4500, 4501..4545, 4546..4590, 4591..4635, 4636..4680, 4681..4725, 4726..4770, 4771..4815, 4816..4860, 4861..4905, 4906..4950, 4951..4995, 4996..5040, 5041..5085, 5086..5130, 5131..5175, 5176..5220, 5221..5265, 5266..5310, 5311..5355, 5356..5400, 5401..5445, 5446..5490, 5491..5535, 5536..5580, 5581..5625, 5626..5670, 5671..5715, 5716..5760, 5761..5805, 5806..5850, 5851..5895, 5896..5940, 5941..5985, 5986..6030, 6031..6075, 6076..6120, 6121..6165, 6166..6210, 6211..6255, 6256..6300, 6301..6345, 6346..6390, 6391..6435, 6436..6480, 6481..6525, 6526..6570, 6571..6615, 6616..6660, 6661..6705, 6706..6750, 6751..6795, 6796..6840, 6841..6885, 6886..6930, 6931..6975, 6976..7020, 7021..7065, 7066..7110, 7111..7155, 7156..7200, 7201..7245, 7246..7290, 7291..7335, 7336..7380, 7381..7425, 7426..7470, 7471..7515, 7516..7560, 7561..7605, 7606..7650, 7651..7695, 7696..7740, 7741..7785, 7786..7830, 7831..7875, 7876..7920, 7921..7965, 7966..8010, 8011..8055, 8056..8100, 8101..8145, 8146..8190, 8191..8235, 8236..8280, 8281..8325, 8326..8370, 8371..8415, 8416..8460, 8461..8505, 8506..8550, 8551..8595, 8596..8640, 8641..8685, 8686..8730, 8731..8775, 8776..8820, 8821..8865, 8866..8910, 8911..8955, 8956..9000, 9001..9045, 9046..9090, 9091..9135, 9136..9180, 9181..9225, 9226..9270, 9271..9315, 9316..9360, 9361..9405, 9406..9450, 9451..9495, 9496..9540, 9541..9585, 9586..9630, 9631..9675, 9676..9720, 9721..9765, 9766..9810, 9811..9855, 9856..9900, 9901..9945, 9946..9990, 9991..10035, 10036..10080, 10081..10125, 10126..10170, 10171..10215, 10216..10260, 10261..10305, 10306..10350, 10351..10395, 10396..10440, 10441..10485, 10486..10530, 10531..10575, 10576..10620, 10621..10665, 10666..10710, 10711..10755, 10756..10800, 10801..10845, 10846..10890, 10891..10935, 10936..10980, 10981..11025, 11026..11070, 11071..11115, 11116..11160, 11161..11205, 11206..11250, 11251..11295, 11296..11340, 11341..11385, 11386..11430, 11431..11475, 11476..11520, 11521..11565, 11566..11610, 11611..11655, 11656..11700, 11701..11745, 11746..11790, 11791..11835, 11836..11880, 11881..11925, 11926..11970, 11971..12015, 12016..12060, 12061..12105, 12106..12150, 12151..12195, 12196..12240, 12241..12285, 12286..12330, 12331..12375, 12376..12420, 12421..12465, 12466..12510, 12511..12555, 12556..12600, 12601..12645, 12646..12690, 12691..12735, 12736..12780, 12781..12825, 12826..12870, 12871..12915, 12916..12960, 12961..13005, 13006..13050, 13051..13095, 13096..13140, 13141..13185, 13186..13230, 13231..13275, 13276..13320, 13321..13365, 13366..13410, 13411..13455, 13456..13500, 13501..13545, 13546..13590, 13591..13635, 13636..13680, 13681..13725, 13726..13770, 13771..13815, 13816..13860, 13861..13905, 13906..13950, 13951..13995, 13996..14040, 14041..14085, 14086..14130, 14131..14175, 14176..14220, 14221..14265, 14266..14310, 14311..14355, 14356..14400, 14401..14445, 14446..14490, 14491..14535, 14536..14580, 14581..14625, 14626..14670, 14671..14715, 14716..14760, 14761..14805, 14806..14850, 14851..14895, 14896..14940, 14941..14985, 14986..15030, 15031..15075, 15076..15120, 15121..15165, 15166..15210, 15211..15255, 15256..15300, 15301..15345, 15346..15390, 15391..15435, 15436..15480, 15481..15525, 15526..15570, 15571..15615, 15616..15660, 15661..15705, 15706..15750, 15751..15795, 15796..15840, 15841..15885, 15886..15930, 15931..15975, 15976..16020, 16021..16065, 16066..16110, 16111..16155, 16156..16200, 16201..16245, 16246..16290, 16291..16335, 16336..16380, 16381..16425, 16426..16470, 16471..16515, 16516..16560, 16561..16605, 16606..16650, 16651..16695, 16696..16740, 16741..16785, 16786..16830, 16831..16875, 16876..16920, 16921..16965, 16966..17010, 17011..17055, 17056..17100, 17101..17145, 17146..17190, 17191..17235, 17236..17280, 17281..17325, 17326..17370, 17371..17415, 17416..17460, 17461..17505, 17506..17550, 17551..17595, 17596..17640, 17641..17685, 17686..17730, 17731..17775, 17776..17820, 17821..17865, 17866..17910, 17911..17955, 17956..18000, 18001..18045, 18046..18090, 18091..18135, 18136..18180, 18181..18225, 18226..18270, 18271..18315, 18316..18360, 18361..18405, 18406..18450, 18451..18495, 18496..18540, 18541..18585, 18586..18630, 18631..18675, 18676..18720

|